The investment gap

A very British problem

Brits hate investing their money.

We have the lowest level of retail investment in the G7. The average household has just 8% of their wealth sitting in stocks.

For some reason, we’ve got this national obsession with buying property. It’s seen as a safe, aspirational investment with strong, consistent returns.

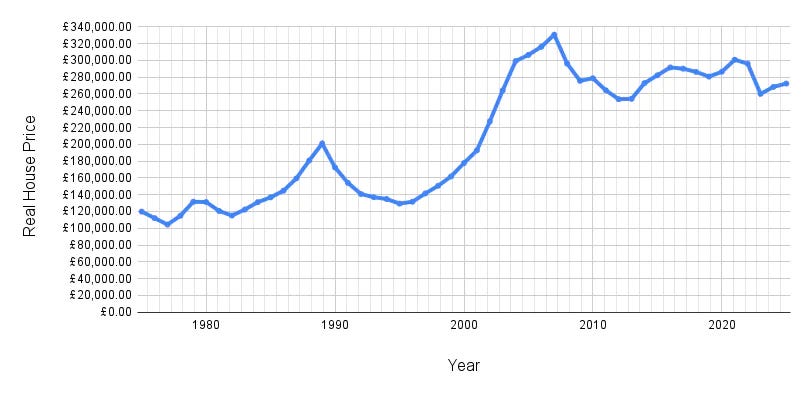

That may have been true in the 20th century - but it is no longer the case. Once you account for inflation, house prices have barely risen over the last ten years - many houses have seen their real term value decrease.

House prices adjusted for inflation

Let’s put the numbers into perspective: if you bought a £200,000 house in 2016 it would today be worth about £270,000. That sounds good - but actually, that hasn’t even kept pace with inflation. You’d need £277,012.41 today to buy as much as £200,000 bought you in 2016.

Instead of buying that house, let’s imagine you had invested that £200,000 into the S&P500 - which is simply the 500 top companies in the US. You would today have £600,000+.

But only 23% of Brits are doing this (compare that to two thirds of Americans who hold stocks). There is inherent risk with investing in stocks, of course, but a long run of historical data shows us that share prices consistently rise over the long-term. There is something in the water in the UK that means Brits can tolerate the risk of an investment in property, but won’t tolerate the risk of an investment in stocks.

This isn’t financial advice, but I will say this - investing is incredibly easy. You don’t need to choose companies, you don’t need to buy and sell regularly. You just buy and hold.

Almost all investment accounts offer exchange-traded funds: which are baskets of shares you can buy as a group. The risk is lowered because you hold a diversified portfolio: if one company does badly, there are plenty of others that might do well and smooth the turbulence.

No stake

Why is it a problem that Brits don’t invest?

Firstly, growth in Britain has all but stalled. After the 2008 recession, GDP growth essentially slowed to half its previous speed. Other countries see their growth skyrocket: we’ll be lucky to grow the economy 1% this year, India will be eyeing up 7% growth. That means the country isn’t getting richer: less money for public services and infrastructure. And it means we don’t get richer: salaries stagnate and our buying power falls.

Fuelling growth depends on businesses succeeding in Britain. Look at America - the surge of AI companies has created thousands of jobs, made multiple millionaires and billionaires, and attracted huge amounts of overseas investment. The same has not happened here.

Part of the reason we struggle is because there is a lack of capital in the UK. Companies, in particular innovative start-ups, need money: and the UK is short of it. An IPO (Initial Public Offering - a company’s first time selling stocks to the public) should be a moment to get a bunch of cash into the coffers. Two decades ago, companies listing in London raised a total of $50 billion. Now, the exchange struggles to reach $2 billion.

The natural consequence of the lack of capital is that companies move to the US, where there is lots of money floating around. They take their jobs, their tax contributions, their investment over there.

Reversing this trend means getting more money into the stock market, particularly into British stocks: individuals choosing to invest their money rather than let it sit and shrivel in a savings account is a big part of that.

But secondly, the lack of retail investment means that Brits have less of a stake in the success of the country.

If Rachel Reeves’ plan works, and the economy grows, some Brits might get lucky and see the real-terms impact of this: a payrise, or a new job. But the majority won’t see any meaningful change in their life at all. But if they held shares, they would quite literally have a tie to the fortunes of the nation. When Britain does well, we’d all do well with it.

(This would have the added bonus of disincentivising voters from choosing kamikaze missions like Brexit or Truss: there is a real financial incentive to choose good leaders, not entertaining ones.)

Property ownership was seen by Thatcher as a way to give people a stake in the economy. As property becomes a riskier investment, and one that is out of reach for more people, buying a stake in British business can offer a new route to having a stake in the country.

How to start investing

I do have to emphasise that none of this is financial advice: this is about a need at a national level to increase participation in the stock market. You can do whatever you want with your money.

But if you’re reading this as one of the 75% of Brits who doesn’t invest, and fancies starting, here’s a very quick guide. Remember that investing does carry risk - just like any investment. But the historical returns have been substantial and consistent.

Open a Stocks and Shares ISA: you can put away up to £20,000 a year and not pay any tax on your gains. Money Saving Expert recommends platforms here.

Select funds to invest in. You can invest in individual companies (like buying shares in Tesla) but they are typically more volatile, and the risk is higher. Many platforms offer themed funds.

Try not to take the money out until you reach your savings goal. There will be stock market crashes where the value of your investments fall: the key is not to be spooked.

That’s it! Reading the FT and commenting on the stock market performance at dinner parties is optional, but feel free.

It really is hard to discern why more people in this country don’t do this. The government has introduced plenty of tax advantages to investing. Some have theorised that the media overstates the risk of the stock market, or the language used in financial ads is too jarring, or that we need more financial education in schools (the government is working to address those last two points).

I think we need more, though: a cultural change, not just a policy change. Just like home ownership was encouraged and normalised in the 80s, we need to do that with share ownership today.

Very interesting read. Your points make it incredibly clear that paying off a low interest rate mortgage by taking money out of an investment vehicle, is madness!

Think its a good idea to teach this at school